The VA loan is one of few mortgage products that offer qualifying borrowers 100% financing. The low down payment opportunity available through this mortgage can make it possible for valued service members and their families to lay down roots.

If you’re a service member thinking about purchasing with a VA loan, consider the benefits of putting some money together before coming to the deal table empty-handed.

There are a few reasons you may want to put down money even if it’s not required.

A Down Payment Can Lower the Funding Fee

A key reason to consider a down payment is it can decrease your funding fee. The VA loan doesn’t require mortgage insurance, but there is a funding fee charged to borrowers to keep the program running for other veterans.

Disabled veterans and spouses of veterans who died on active duty may be exempt from the funding fee. You should expect to pay this fee unless you’re part of an exempt class.

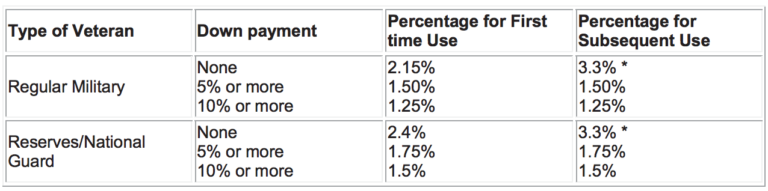

Funding fees are charged based on tiers depending on your down payment, and whether the VA loan you’re obtaining is your first or subsequent VA loan.

The funding fee ranges from 1.25 percent to 2.15 percent for first-time homebuyers who fall into the “regular military” category. The fee range is 1.25 percent to 3.3 percent for subsequent home loans.

Fee table is directly from the Veterans Benefits Administration.

You can expect to pay a funding fee of $2,150 per $100,000 if you have no down payment. That fee decreases to $1,500 and $1,250 if you make a down payment of 5 to 10 percent.

The good news is you don’t have to pay the funding fee at closing. You have the option to roll your funding fee into the home loan. Keep in mind, rolling the fee into your mortgage can increase your monthly mortgage payment.

A Down Payment Can Lower Monthly Payments

Obtaining 100% financing on your home comes with an immediate benefit. You can buy a home without needing to get the money together upfront. There’s a tradeoff to this benefit.

A higher loan amount will likely mean a higher monthly payment, and interest will cost you more over the life of the loan. If a low monthly payment is important to you (and so is interest savings), bringing some money to the table instead of zero down could be a money-savvy choice.

A Down Payment Gives You Equity in the Home Right Away

It can take you a bit longer to build equity in your home when you don’t make a down payment. This may not be a big deal right away. But in the future, you could need a home equity line of credit or home equity loan for repairs or other expenses. These products may be available to you sooner if you have equity in the home from the onset.

Final Words

A mortgage that requires no down payment can be just the right product to get you into your dream home. There are some instances where veterans may want to put some money down even if it’s not necessary.

With that said, no two homebuying situations are the same. If you’re not sure what the best move is for you, one of our loan officers can review mortgage options and various down payment scenarios with you.

*Atlantic Coast Mortgage, LLC is not affiliated with or acting on behalf of or at the direction of Veterans Administration, the Federal or State Government.

Rates change daily and will vary depending on your unique situation. For a FREE customized quote, please enter the location (City/State) for the property you're trying to Purchase or Refinance!

Get Your Free Rate Quote!

Rates change daily and will vary depending on your unique situation. For a FREE customized quote, please enter the location (City/State) for the property you're trying to Purchase or Refinance!