If you’ve ever wondered, “where does money come from?” then chances are you’ve googled down a rabbit hole and found the Federal Reserve. “The Fed” as they’re affectionately known, has three broad, never-ending goals: maximum employment, stable prices, and moderate long-term interest rates. Now, those are some big goals, and the Fed has a variety of tools at their disposal to pursue them—but big goals tend to call for big tools. So much so that anything the Fed does (or doesn’t) do tends to ripple out and affect the world at large.

The world, such as… mortgage rates. Whether you’re a would-be homebuyer, a could-be refinancer, or just midway through a google-rabbit-hole, it pays to have a general idea of what the Fed’s latest monthly meeting means for mortgage rates. We’ll break it down together.

What has the Fed been doing?

Recapping what the Fed does: They are the custodians of the U.S. economy. Whenever there’s a downturn in some way, they step in to attempt to get things back on track.

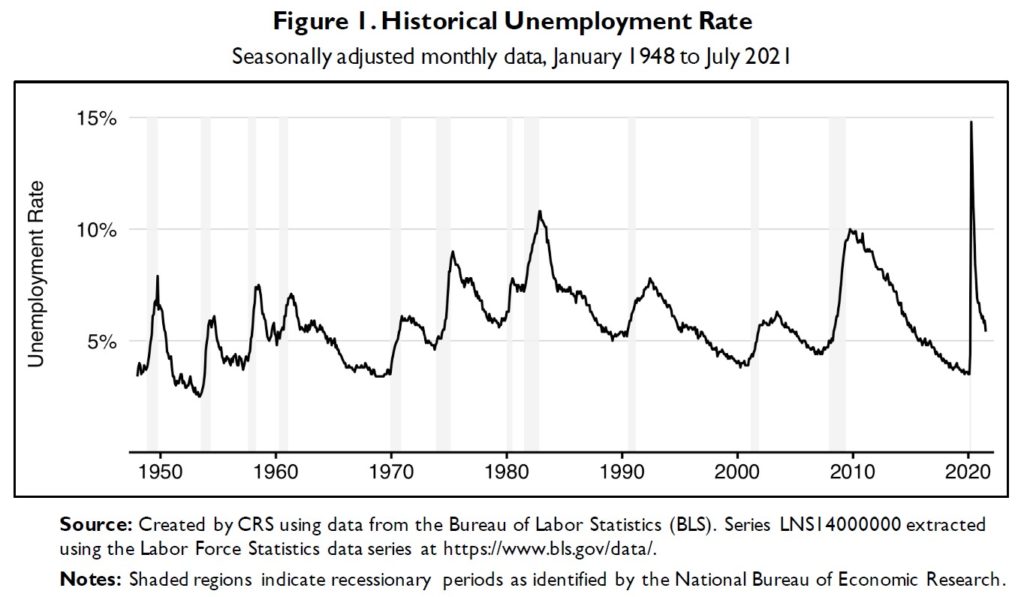

Now, at the tail end of February 2020, COVID-19 went international (if you’re reading this, chances are you remember it). As of early March, the global economy essentially shut down for fear of infection—and the U.S. stock market plummeted. Unemployment went from 3.8% in February to 14.8% in April. This all very easily counts as “a downturn.”

Luckily, the Fed had something of a blueprint for what to do from previous crises. Their response included everything from direct lending to state governments and banks and corporations, to backstopping money market mutual funds and making U.S. dollars available to other central banks via international swap lines. Their biggest moves to focus on for our sake are:

“How Low Can You Go?” Interest Rates – Not only did the Fed slash the federal funds rate (the rate banks pay to borrow from each other overnight) to historically low markers (0% to .25% is low!), but they also employed something called Forward Guidance. When you have colossal sway over the financial world, even just saying what you’re going to do next can be a tool. The Fed announced they would keep rates low “until labor market conditions reached levels consistent with the Committee’s assessment of maximum employment, and inflation is on track to exceed 2% for some time.” Loosely translated: The Fed announced rates were going to be low for as long as they needed to be.

“There Is No Such Thing as a Price Tag” Purchasing – This is “the big gun” in the Fed’s arsenal. The Fed can purchase treasury- and mortgage-backed securities to help keep markets running smoothly. The Fed announced that purchasing was going to be open-ended—AKA there was no limit to how much they could spend.

“The Money Printer Goes Brrrrrrr” Cash Injection – In the same theme, the Fed also offered the repo markets (where firms borrow and lend cash & securities short-term) unlimited amounts of money. This was critical because any disruption in the repo market inevitably affects the Federal funds rate, which is the primary way the Fed achieves their price stability and employment mandate.

Summed up neatly: The Fed flipped a switch and flooded the world with money, right as the world needed it most. Not only that, but they reassured the world that they would keep doing this for the foreseeable future. This is the largest asset purchase plan in the Fed’s history, which also makes it a somewhat unconventional action by the Federal Reserve. Economically speaking, the COVID crisis could have been so much worse.

Well, what’s changed?

As of writing, it’s the start of January 2022, and the landscape is different. Unemployment currently sits at 3.9%, and inflation has just been announced at 7%—the highest it’s been in roughly 40 years. The Fed, recognizing that the situation had changed back in November 2021, officially announced that they were going to begin tapering.

Wait, what’s a “taper?”

The formal definition of taper is “a gradual or incremental reduction.” If you were a runner, it would be gradually training less so that you’re feeling fresh for a big race. If you were a tailor, it would mean incrementally tightening pant legs as they approach the ankle.

In the Fed’s case, it means they’re going to gradually purchase less securities and ultimately means inflation should fall, but will inevitably have effects on all financial markets.

Okay, but what does that mean for mortgage rates?

Immediately, it might mean very little. Thanks to Forward Guidance, the Fed had been signaling that a taper was on the horizon for some time. The world has had plenty of time to wrap its head around the idea, so the chance of a “taper tantrum” is theoretically less likely.

With regards to a longer timeline, there’s a runway for things to change. And while it might be easy to correlate bond prices changing with the Fed’s actions, the relationship between the Fed and mortgage rates is complicated—it’s not as clear-cut as when the Fed just says, “the federal funds rate is now this.” Again, the Fed’s actions ripple out and touch everything. Historically speaking, this blog might’ve been about how the Fed’s actions would eventually (inadvertently) affect mortgage rates, i.e., “The Fed has done this, so bonds are now this, which means banks and investment firms are now doing this, so mortgage rates are likely to do this.”

But, one big way the Fed currently touches mortgages: Remember that since June 2020, the Fed has been buying $80 billion of agency mortgage-backed securities every month as part of its security purchases (that’s “purchasing securities to keep markets running smoothly” in action). And a quick reminder that a mortgage-backed security is a bundle of home loans turned into an asset-backed security and ultimately traded by investors. The Fed vacuuming all of these up off the market had driven rates to limbo-levels of low.

Now, generally speaking, yields rise when the biggest buyer in the marketplace stops buying, and for just about all of 2020 and 2021, there was no bigger buyer than the Federal Reserve. While we are a few months into the taper, and the Fed has pushed the timeline for concluding their purchases up from June 2022 to March 2022, there is still plenty of runway for the Fed to draw down their purchases. A fast taper of the Fed’s purchasing would very likely push mortgage rates up, and a slow taper could potentially help keep mortgage rates relatively lower for some time to come.

The TLDR version is this:

Are there any other Fed actions that affect mortgage rates?

Well, now that you mention it, yes. The Fed tapering its purchases is typically one-half of the tried-and-true response. The other half is what’s called a rate hike. We already mentioned that the Fed decides the federal funds rate and that this is the rate that banks pay to borrow from each other overnight. A rate hike is exactly what it sounds like—the Fed raises, or hikes, the federal funds rate.

Changes to the federal funds rate might move the rate on the 10-Year Treasury; it depends on what banks and investment firms ultimately choose to do in response to the federal funds rate changing. And remember—fixed-mortgage rates tend to match the 10-year Treasury rate. If the rate for the 10-Year Treasury goes up, fixed-mortgage rates tend to do the same.

As of January 2022, the Fed has broadcast their plan for three rate hikes in 2022, but several commercial banks estimate there will be at least four.

So what should I do regarding my mortgage?

If you were thinking about refinancing to take advantage of current mortgage rates, there’s a little bit more urgency to do so now than there was this time last year. We’re not guaranteeing rates go up—guaranteeing anything in finance is a fool’s errand—but the main variables that have made mortgage rates low up till now seem to be coming to an end. It’s more likely rates go up than they go down from here.

Your Next Steps…

… Should start with trusted guidance from someone who knows their stuff. And while there is an entire industry out there worth considering, the right choice may be right in front of you at this exact moment. Atlantic Coast Mortgage, LLC has over a decade of results to its name, thanks to a roster of mortgage professionals all singularly focused on elevating the homebuying experience. That’s why we’re so confident we can get you from “what’s next?” to “welcome home.”

This is an advertisement and is not a commitment to lend. Contact lender to discuss the loan programs, payment and term options available specifically for you and your needs.

Rates change daily and will vary depending on your unique situation. For a FREE customized quote, please enter the location (City/State) for the property you're trying to Purchase or Refinance!

Get Your Free Rate Quote!

Rates change daily and will vary depending on your unique situation. For a FREE customized quote, please enter the location (City/State) for the property you're trying to Purchase or Refinance!